“`html

State-Level Capital Gains Taxation: A Closer Look at the 2024 Landscape

As the new year unfolds, taxpayers and policymakers alike turn their attention to the intricacies of capital gains taxation. The Tax Foundation has recently shed light on the varying approaches to taxing capital gains across the United States, highlighting the disparities between federal and state tax codes.

Capital gains, the profits from the sale of assets, are a fundamental element of taxable income. However, a critical point of contention arises from the method of calculating these gains. The original purchase price, or tax basis, is subtracted from the selling price without adjusting for inflation, leading to taxes on nominal increases in wealth. This often results in taxpayers shouldering a burden for what is, in essence, a net loss when inflation is accounted for.

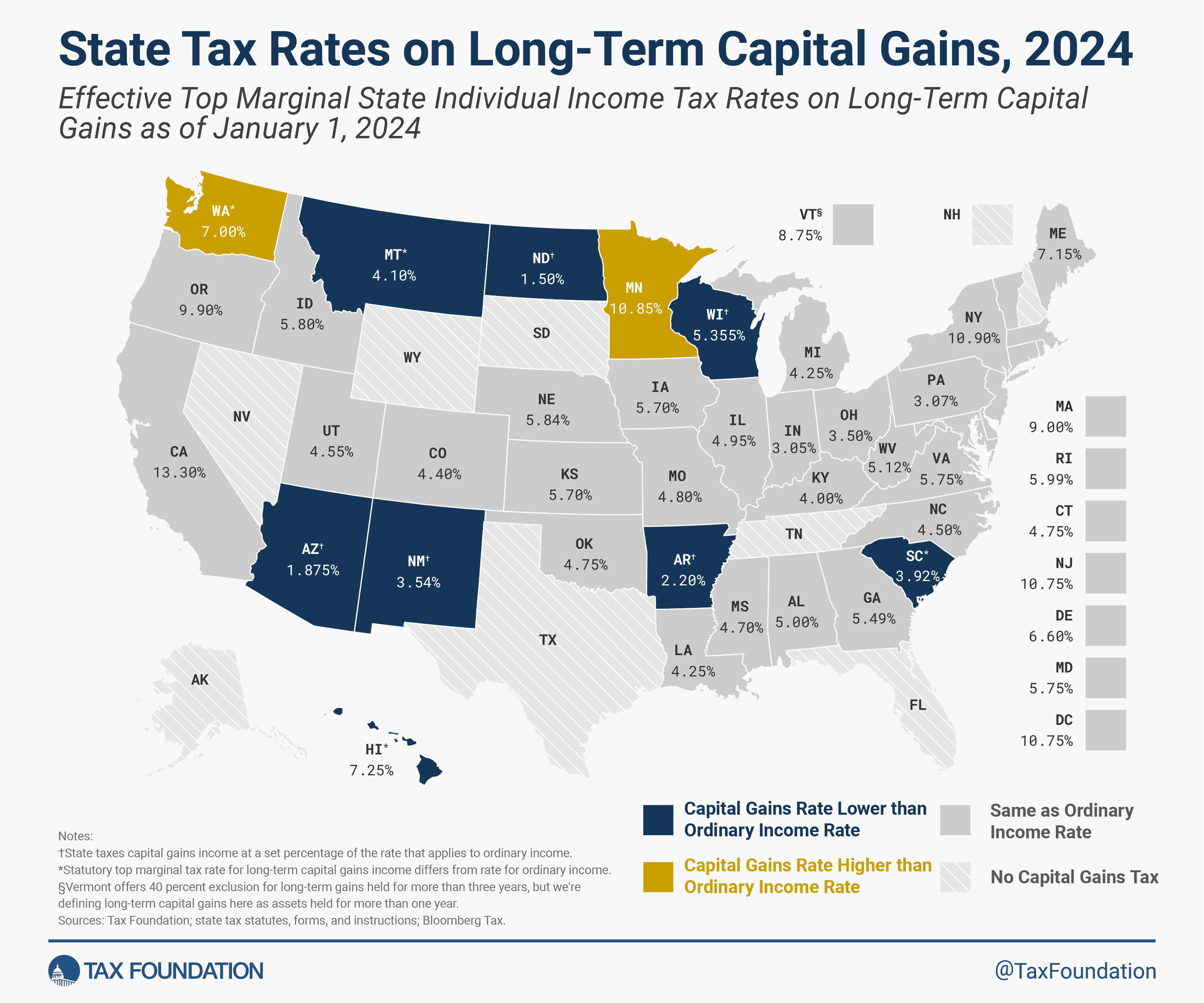

The federal government offers some relief by taxing long-term capital gains—those on assets held for over a year—at lower rates than ordinary income. Taxpayers may fall into brackets of 0 percent, 15 percent, or 20 percent for these gains. Yet at the state level, such accommodations are less common. Thirty-two states and the District of Columbia tax capital gains as ordinary income, with Minnesota and Washington imposing even higher rates on certain capital gains.

Conversely, only eight states emulate the federal model by applying lower effective rates to long-term capital gains. Seven states sidestep this issue entirely by not levying an individual income tax at all, while New Hampshire taxes only interest and dividends income.

Advocates argue that more states should follow suit in applying lower rates to long-term capital gains or offering exclusions for a portion of these gains. This would better reflect the real value of assets after accounting for inflation. Furthermore, robust deductions for capital losses are encouraged to provide a fairer tax landscape.

Despite these measures, it’s important to recognize that capital gains taxes often represent a form of double taxation. For instance, when individuals invest in stocks with post-tax income, any growth reflects corporate profits already diminished by corporate income taxes. When these shares are sold, the gains are taxed again, despite being reduced by prior corporate taxation.

Lower rates on long-term capital gains may appear preferential at first glance. However, considering inflation and pre-existing layers of taxation reveals a more complex scenario. State policymakers are urged to consider these factors to avoid overtaxation of capital gains income and encourage savings and investment vital for economic health.

As tax policies continue to evolve, staying informed remains crucial for both taxpayers and those shaping future legislation.

“`