European Stocks Outshine Wall Street Amid Currency Movements

In a remarkable display of resilience, European stocks were poised to outperform their Wall Street counterparts on Friday, with a particular surge in exporter shares. This uptick comes as Europe’s major currencies faced a downturn against a robust dollar, fueled by expectations that the U.S. Federal Reserve would maintain elevated interest rates.

The Stoxx Europe 600 index, a broad measure of shares across the continent, climbed 1.1 percent in the morning session. The weakening of the euro proved advantageous for the domestic valuation of exporters’ earnings in dollars. London’s benchmark FTSE 100 index also enjoyed a 1.3 percent rise, bolstered by robust performances in global mining and oil stocks.

Contrastingly, futures markets hinted at a subdued opening for Wall Street, with the S&P 500 index projected to open 0.1 percent lower and Nasdaq 100 futures indicating a 0.3 percent decline. This comes as Wall Street braces for its second consecutive weekly fall, amidst a recalibration of U.S. rate-cut expectations following unexpectedly high consumer price data earlier in the week.

Investors are recalibrating their expectations for the Fed’s rate trajectory, with current money-market pricing suggesting a reduction of approximately 45 basis points in the main funds rate this year. Despite starting the year with anticipations of around 150 basis points in cuts, traders are now facing U.S. interest rates at a 23-year peak of between 5.25 and 5.5 percent.

Marcelo Carvalho of BNP Paribas highlighted the challenges ahead for the Fed compared to the European Central Bank (ECB), given the robust U.S. labor market and economy. Meanwhile, the eurozone is witnessing a decline in inflation towards the ECB’s target as growth and bank lending slow within the bloc.

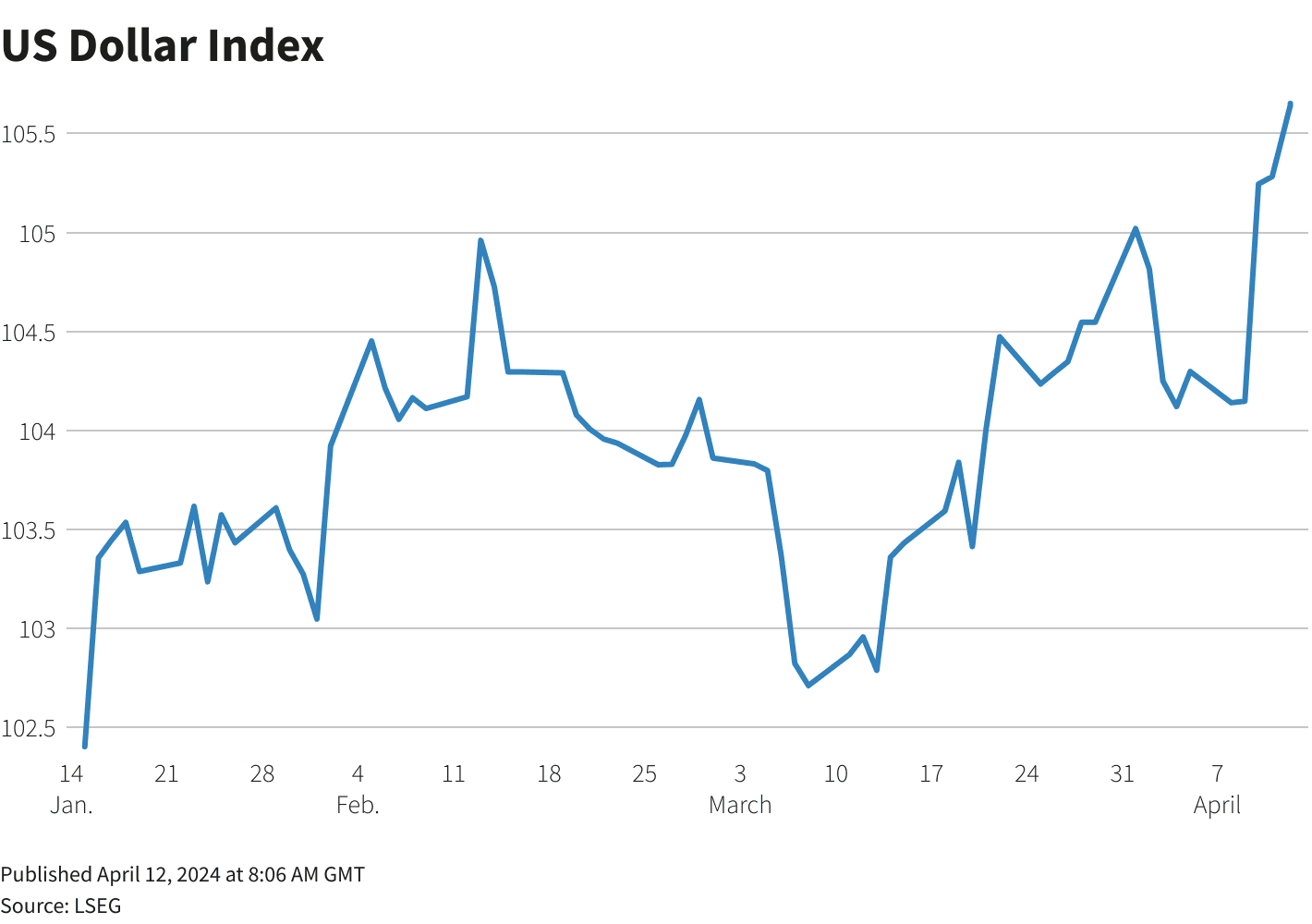

The dollar’s strength was evident as the dollar index rose 0.5 percent to 105.82, marking a weekly gain of 1.5 percent against a basket of major peers. The Japanese yen reached a 34-year nadir against the dollar, sparking speculation about potential intervention from Tokyo to bolster the currency.

Amidst these currency fluctuations, the ECB has signaled a potential rate cut in June from its current record high of 4 percent, while the Bank of England is also expected to reverse its aggressive monetary tightening sooner than anticipated. These developments have exerted pressure on both the euro and sterling, with both currencies hitting multi-month lows against the dollar.

As markets digest these monetary policy signals and their implications for currencies and stocks, investors continue to navigate an intricate landscape shaped by central bank decisions and economic indicators from around the globe.