Stable Outlook for Cyprus Despite Geopolitical Concerns

Morningstar DBRS has reaffirmed Cyprus’s sovereign ratings, acknowledging the country’s robust economic performance while also highlighting its susceptibility to geopolitical events and the limitations imposed by its service-centric economy. The agency maintained the long-term foreign and local currency issuer ratings at BBB (high) and the short-term ratings at R-1 (low), with a stable trend forecast.

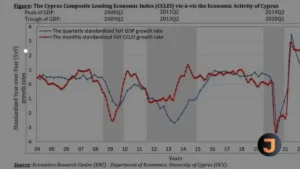

The stable trend reflects a balance between positive economic and fiscal progress and potential risks. Cyprus’s real GDP growth was a solid 2.5% last year, driven by strong private consumption and investment. This growth has had a positive impact on fiscal outcomes, with the public debt-to-GDP ratio falling to 77.4% in 2023 from 85.6% in the previous year.

Despite these positive indicators, Cyprus faces external risks such as the ongoing conflict in Ukraine and potential trade disruptions in the Red Sea. These could affect government revenues and increase expenditure pressures.

The country’s creditworthiness is bolstered by a stable political climate, prudent fiscal management, and a favorable government debt profile. However, challenges persist, including a high volume of non-performing loans within the banking sector and lower labor productivity compared to the EU average.

Economic Drivers and Fiscal Management

Tourism and ICT relocations have significantly contributed to Cyprus’s economic growth. The rebound in tourist arrivals and expansion of the ICT sector have been particularly noteworthy, although financial sanctions on Russia in spring 2023 have impacted business services. The Central Bank of Cyprus projects a moderate increase in real GDP growth in the coming years.

Investments are expected to be spurred by Next Generation EU funds and major projects in tourism and real estate. Nevertheless, labor productivity remains a concern, with Cyprus’s GDP per person employed at only 87.6% of the EU27 average in 2022.

Budgetary pressures are anticipated due to adjustments in living allowances, deficits in the State Health Organisation, and expansions of state asset management company KEDIPES. KEDIPES’s initiative to acquire primary residences used as collateral in non-performing loans aims to support vulnerable households but has yet to be reflected in budgetary projections.

Debt Reduction and Interest Expenditure

Cyprus’s government debt-to-GDP ratio continues its downward trajectory, with projections suggesting a further significant decrease by 2025. The reduction in debt, coupled with favorable debt dynamics, is expected to offset the impact of rising interest rates.

The European Commission predicts a slight decline in general government interest expenditure. A favorable debt maturity profile and a substantial government cash buffer mitigate short-term funding risks. However, potential economic shocks or liabilities from the banking sector remain concerns for public finances.

The recent presidential election has not led to significant policy shifts, particularly regarding fiscal policy. The success of Cyprus’s recovery plan hinges on the government’s legislative support. While governance indicators have declined, EU membership continues to be an anchor for institutional quality. The prospects for reunification talks remain uncertain, according to Morningstar DBRS.